1. 引言

亚式期权是一种强路径有关的期权,其支付函数与到期日之前的时间区间内原生资产价格的平均值有关。于是亚式期权可以分为两类:算术平均亚式期权和几何平均亚式期权 [1] 。对于几何平均亚式期权,很容易得到闭合解(closed-form solution),相应的定价问题可以解决。由于不清楚相关对数正态分布的随机变量之和的分布,算术平均亚式期权的定价就显得非常困难,目前还没有任何的闭合解 [1] [2] 。而实际交易的亚式期权大多是离散采样的,所以对于这一类期权的研究相当有意义。目前有许多方法去研究离散采样的算术亚式期权,包括解析逼近、上下界估计、数值计算和拟解析方法等 [2] - [6] 。假设原生资产具有均值回归和带跳的性质,Chung和Wong [7] 得到了离散的算术平均亚式期权的解析定价公式。当原生资产价格在与时间有关的Lévy过程下演化时,Yamazaki [8] 利用Gram-Charlier展开方法得到了离散和连续采样的亚式期权定价的近似公式。

本文我们将研究由Curran [3] [4] 和Nielsen [5] 给出的通过上下界估计方法得到的算术亚式期权两类近似计算公式,着重分析它们的误差和优劣。在此基础上我们发现Nielsen的近似公式相对较为精确。

2. 近似公式及讨论

考虑风险中性世界,原生资产价格 服从如下几何布朗运动

服从如下几何布朗运动

(1)

(1)

其中 是标准的布朗运动,

是标准的布朗运动, 是无风险利率,

是无风险利率, 表示支付红利,

表示支付红利, 表示波动率。这里

表示波动率。这里 假设为常数。期权到期日设为

假设为常数。期权到期日设为 ,交割价设为

,交割价设为 ,离散采样个数设为

,离散采样个数设为 。

。

下面我们先叙述Curran和Nielsen的期权定价公式,然后给出Curran公式的证明(文献 [3] 中没有给出具体推导过程),它将有助于分析误差来源。

定理1 (Curran定价公式 [3] [4] )离散采样的算术平均亚式期权在时刻 时的定价公式为

时的定价公式为

(2)

(2)

其中

这里 表示

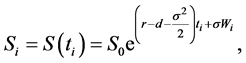

表示 时刻资产价格,

时刻资产价格, 是第一个采样时间,

是第一个采样时间, 表示采样时间间隔,

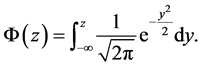

表示采样时间间隔, 是标准的正态分布函数:

是标准的正态分布函数:

证明 由(1)和Itǒ公式,我们有

这里 服从正态分布

服从正态分布 。算术平均价格和几何平均价格分别为

。算术平均价格和几何平均价格分别为

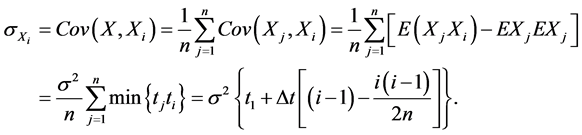

令随机变量 ,显然

,显然 的期望和方差分别为

的期望和方差分别为 。引入

。引入 ,于是

,于是 容易验证随机变量

容易验证随机变量 是正态分布,期望和方差分别为

是正态分布,期望和方差分别为

随机变量 和

和 的协方差为

的协方差为

注意到 和

和 是双变量正态分布,我们得到

是双变量正态分布,我们得到

从而 的条件分布是对数正态分布

的条件分布是对数正态分布

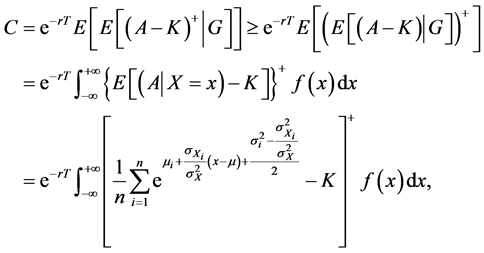

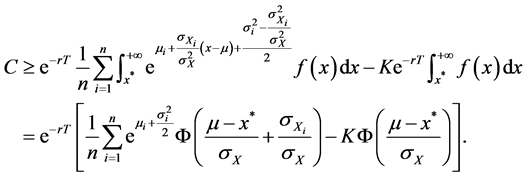

于是亚式看涨期权的定价公式为

(3)

(3)

其中 是随机变量

是随机变量 的正态密度函数。

的正态密度函数。

记

(4)

(4)

在(4)式推导中利用了恒等式

以及下述重要关系式

(5)

(5)

用 逼近

逼近 ,注意到

,注意到 ,

, 的零点可以用下述方式近似

的零点可以用下述方式近似

(6)

(6)

于是,方程(3)可写为

证毕。

从上面证明过程可知,Curran公式事实上是亚式看涨期权的下界 的逼近。

的逼近。

而且,根据公式(4)和(6),这个近似是有误差的。特别当到期日 固定时,由(5)式可以看出,定价公式的误差对波动率非常敏感。

固定时,由(5)式可以看出,定价公式的误差对波动率非常敏感。

下面的算术平均亚式期权定价近似公式由Nielsen [5] 给出。

定理2 (Nielsen公式)

(7)

(7)

其中

由Nielsen公式的证明过程(参见[5] )可以看出,该公式就是期权定价下界 ,这里随机变量

,这里随机变量 是标准的正态分布。而前面给出的Curran公式是期权定价下界

是标准的正态分布。而前面给出的Curran公式是期权定价下界

的一种近似,其中随机变量 是几何平均价格。所以通过上述讨论,可以看出Nielsen公式比Curran公式更加接近真实解。

是几何平均价格。所以通过上述讨论,可以看出Nielsen公式比Curran公式更加接近真实解。

基金项目

安徽省自然科学基金(1408085MA01)。