1. 引言

目前,中国是全球最大的棉花生产、贸易和消费国。但我国棉花生产与经营分散,现货市场不规范,在进出口贸易中也不时出现“高买低卖”的不正常现象。为向涉棉企业提供避险工具,提高中国作为重要的棉花市场在国际上的整体影响力,棉花期货于2004年6月1日在郑州商品交易所上市交易。

本文通过分析棉花的期货市场和现货市场之间的价格传导关系,从而判断我国棉花期货市场功能发挥的程度以及对现货市场的影响程度。

2. 文献综述

刘庆富(2006)[1] 利用日收盘价格,借助于信息共享模型与波动溢出效应模型对我国农产品的大豆和小麦期货市场与现货市场之间的价格发现和波动溢出效应进行了研究,并表明:大豆期货市场与现货期货市场价格之间存在双向引导关系,而小麦市场只存在期货价格对现货价格的单项引导关系;大豆和小麦的期货市场与现货市场之间均存在双向的波动溢出关系。

李惠茹(2006)[2] 利用收盘价格,借助信息共享模型、方差分解和脉冲响应函数等研究我国棉花期货市场与现货市场之间的价格关系,并表明:棉花期货价格和现货价格之间存在双向引导关系和长期均衡关系,期货价格对现货价格具有预测作用。

祝合良(2007)[3] 通过研究铜、大豆、小麦3个品种国内外期货价格之间的关系,发现铜、大豆国内外期货价格之间存在长期均衡关系并相互影响,但是小麦国内外期货价格之间并不存在长期均衡关系,说明铜、大豆期货价格信号对国际期货和现货市场产生了很大影响,但是小麦期货价格信号对国际期货和现货市场产生的影响还非常有限。

从我国期货市场与现货市场之间价格关系的研究来看,期货市场和现货市场之间的价格是具有一定的传导性的。研究期货市场与现货市场的价格传导性对于我国证券市场乃至金融市场的健康发展有着非常重大的意义。

3. 样本选取

本文以郑州期货交易所棉花期货的日交易数据为研究对象[4] 。棉花期货合约选取2011年9月16日至2013年9月12日交易数据,数据来源于郑州商品交易所网站,以当日收盘价为准。

棉花现货价格采用中国棉花328指数,记为CC,数据来自于郑州商品交易所网站[5] 。数据如表1。

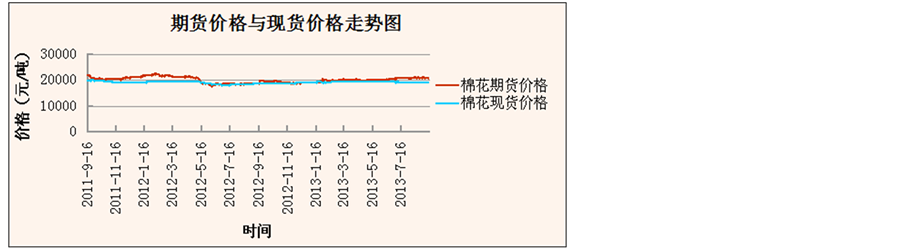

2011年~2013年棉花期货与现货价格的变化情况(如图1):

1) 棉花的现货价格波动较为平稳。

2) 棉花的期货价格的波动则分为三个阶段:第一阶段价格波动性上升,第二阶段价格略有波动性下

Table 1. Primary data

表1. 原始数据

Figure 1. Changes of cotton price in futures market and cash market from 2011 to 2013

图1. 11~13年棉花期货与现货价格的变化情况

降,第三阶段价格持续上升。

3) 棉花的现货价格与期货价格的变化具有较高的一致性,且期货价格的波动性更大;期货价格在绝大部分观察日中都高于现货价格;期货价格比现货价格先达到最低点且稍高于现货价格最低点。

4. 实证分析

本文拟通过一下步骤对棉花期货市场与现货市场之间的价格关系进行研究。

1) 平稳性检验

在进行格兰杰检验和误差修正模型分析时,对原始数据进行了一定的处理。利用Eviews6.0分别对 ,

, 时间序列变量进行ADF平稳性检验,由表2的检验结果可以看出,

时间序列变量进行ADF平稳性检验,由表2的检验结果可以看出, 原序列不平稳,经过一阶差分后均平稳,表明棉花期货价为一阶单整序列,而

原序列不平稳,经过一阶差分后均平稳,表明棉花期货价为一阶单整序列,而 原序列平稳,则棉花现货价格为平稳序列。

原序列平稳,则棉花现货价格为平稳序列。

2) 协整检验

EG二阶段分析法的步骤可归结为:a) 用OLS法对变量进行协整回归;b) 用ADF法对回归残差进行平稳性检验。如为平稳序列,则二变量存在协整关系。反之,协整关系不成立。协整回归的结果如下,

对残差序列et的平稳性检验结果如表3所示,et为平稳序列,则LNFT和LNPT存在协整关系,表明两者存在长期均衡关系。

3) 格兰杰因果检验

表4为滞后阶数等于1时的Granger因果检验结果,检验结果接受 不是

不是 的格兰杰原因拒绝了

的格兰杰原因拒绝了 不是

不是 的格兰杰原因的原假设。表明现货价格不是期货价格的格兰杰原因,而期货价格的变动会引起现货价格波动[6] 。

的格兰杰原因的原假设。表明现货价格不是期货价格的格兰杰原因,而期货价格的变动会引起现货价格波动[6] 。

4) 误差修正模型

尽管 和

和 之间存在长期均衡关系,但从短期来看,可能会存在非均衡情况,为了使模型能够

之间存在长期均衡关系,但从短期来看,可能会存在非均衡情况,为了使模型能够

Table 2. ADF unit root test

表2. ADF单位根检验

注:检验形式(C, T, K)分别表示所设定的检验方程含有截距项、时间趋势项以及所选的滞后期数,N指不包括截距项或时间趋势项。*/**/***分别表示在10%,5%和1%的水平下显著。

Table 3. Stationary test residual sequence of et

表3. 残差序列et的平稳性检验

注:***表示在1%的水平下显著。

Table 4. Granger causality test results

表4. Granger因果检验结果

反映短期内的动态调整,建立误差修正模型如下:

和

和 的系数均较小,表明期货和现货价格的短期相关性不大。棉花期货市场和现货市场发生价格的短期变化时,误差修正项系数为负,当期货价格偏离均衡位置时,误差

的系数均较小,表明期货和现货价格的短期相关性不大。棉花期货市场和现货市场发生价格的短期变化时,误差修正项系数为负,当期货价格偏离均衡位置时,误差

修正项能使现货价格以0.63%的调整力度偏离长期均衡状态,但修正速度很慢。

5. 结语

由以上分析,我国棉花期货市场价格和现货市场价格在长期呈现出较为一致的波动趋势,并保持比较稳定的长期均衡关系,这就为套期保值交易提供了前提条件。

但目前棉花期货价格对现货价格尚未形成引导关系,表明我国棉花期货市场的价格发现功能仍不显著。实证表明,我国棉花期货市场成立近10年来,期货市场价格发现功能已经初步具备,但有待于进一步完善。

NOTES

*通讯作者。