摘要: 对期货市场的价格进行合理地预测,可以规避风险,获得收益。本文利用支持向量机(SVM)回归、决策树(RPART)回归、Bagging回归、Boosting回归、随机森林(Random forest)回归五种数据挖掘模型对锌期货的价格进行预测,预测结果良好,对一个月后锌期货价格变动方向的准确率在60%以上。

Abstract:

Predicting futures market price reasonably can avoid risks and get benefit. In this paper, we used five kinds of data mining models—support vector machine (SVM) regression, decision trees re-gression, bagging regression, boosting regression, random forests regression—to predict zinc fu-tures price. It has got good results, whose accuracy rate can reach above 60% for predicting zinc futures price change direction within one month.

1. 引言

期货市场作为现货市场的重要组成部分,对现货市场的价格具有指导和发现功能,对期货市场的价格进行预测,不仅能够通过套期保值的方式规避风险,还能利用对期货价格的预测,进行投机套利活动,获取经济收益。因此,本文利用五种数据挖掘模型,利用锌期货的基本面数据、行业数据以及国内外宏观经济数据,对未来一个月、两个月、三个月、六个月期货锌价格的涨跌方向进行预测。

数据挖掘算法诞生于20世纪末,是一种全新的智能分析技术和方法,具有非常广阔的应用和发展前景。自诞生以来,数据挖掘算法就受到了理论界和实务界的广泛关注,它指的是通过数据挖掘技术从大量数据中提取出隐含在其中的规律,通过对一系列训练集中的样本数据进行分析,生成一定的规则,并将这规则进行推广运用于测试及过程中。

Mcclean, Scotney和Shapcott (2002) [1] 将遗传算法引入到分析模型中,对指数化的投资组合进行优化,得到了一定的效果;Hassan和Nath (2007) [2] 提出了一种基于机器学习的股票价格预测方法,采用了连续的隐马尔科夫模型,将股票的日开盘价,最高价,最低价与收盘价作为模型输入,预测股票的未来日收盘价;杨国梁、赵社涛、蓝柏雄(2001) [3] 利用证券分析技术和随机游走模型对中国金融市场进行分析,得出我国金融市场的证券收益存在可预测成分的结论;冯建、邱菀华(2012) [4] 用一种基于信息熵的神经网络数据分类方法,通过所有神经元的统计权重信息对输入数据进行投票分类。结合关于数据挖掘算法的文献回顾可以发现,近年来国内外学者在金融分析中,对数据挖掘算法的重视程度越来越高,而数据挖掘算法也因为自身的各种优势越来越被大量的金融投资者所接受。

本文选用的数据包含锌的基本面数据、行业数据以及国内外宏观经济数据三个方面,具体数据情况如表1所示。

本文所采用的五种数据挖掘模型分别是支持向量机(SVM)回归、决策树(RPART)回归、Bagging回归、Boosting回归、随机森林(Random forest)回归。

2. 理论方法综述

支持向量回归模型的思路为:构建一个超平面 ,其中,

,其中, 为因变量向高维空间的映射,对支持向量机的回归,需要使得每个观测点y与

为因变量向高维空间的映射,对支持向量机的回归,需要使得每个观测点y与 的离差最小。

的离差最小。

决策树回归模型就是把决策树的思想用于回归的方法中,其分析的思路主要是通过选择一个变量也就是一个属性,这个变量使得通过这个进行分类后的两部分的分别的残差平方和的和最小。然后在分叉的两个节点处,再利用这样的准则,选择之后的分类属性。一直这样下去,直到生成一颗完整的树。

Bagging回归模型、Boosting回归模型、随机森林回归模型都是基于决策树回归的分析思路,Bagging回归模型利用自助法抽样(Bootstrap)的方式,建立更多的回归树,其预测结果为每棵回归树加权平均。

Boosting模型与Bagging回归模型类似,两者的区别在于Boosting回归在自助法抽样时,会根据前一棵回归树的误差,对抽样的权重进行调整,从而对模型进行修正,是的模型的适应能力,进一步提升,模型的拟合效果更加良好。

Table 1. Analysis variables used in the prediction process

表1. 预测过程中所选用的分析变量

随机森林是由随机放回的样本形成的决策树组成的,其特点是这些决策树的每一节点的分割变量不是由所有的自变量竞争产生的,而是由随机选取的少数变量产生,因此不仅产生的每棵决策树的样本是随机的,每棵树的每个节点的产生也是随机的。这些随机产生的决策树数目很大,因此称为随机森林,结果的投票(或平均)是等权的。随机森林在每次自助法(Boostrap)放回抽样后,产生一棵决策树,抽样次数等于树的颗数,随机森林分类算法的关键在于在生成每棵树的时候,每个节点的变量都仅仅在随机选出的少量变量中产生。因此,不但样本是随机的,而且每个节点变量的产生都有很大的随机性。随机森林算法会让每棵树尽量生长,并且不会进行修剪。随机森林算法同样也可以避免“过拟合”现象的产生,同时它并不惧怕维数很大的数据,并且能够对没个变量的重要性进行分析,可以广泛的运用与各种高维数据。

3. 模型分析

下面我们利用模型对一个月后期货锌的价格变动方向进行分析预测,预测过程主要分为以下几个步骤:一、分别利用5种数据挖掘模型,结合本文所选用的分析变量,利用过去索要预测月份前12个月的数据对下一交易月份期货锌的价格变化方向进行预测,分别得出5中模型的预测方向;二、在利用过去15个月作为测试集,采用滚动预测的方式分别计算出5种模型预测的准确率;三、结合5中模型不同的预测结果和5中模型在测试集中的准确率,计算出综合上涨(下跌)概率。

根据上面的分析结果,我们利用训练期间中的所有数据对2015年12月锌期货价格相对于2015年11月的变化情况进行预测,五种模型中,SVM模型判断为上涨、决策树模型判断为上涨、Bagging模型判断为下跌、Boosting模型判断为下跌、Random forest模型判断为下跌。我们选择的测试区间为15个月:2014年9月~2015年11月,经过计算,五种模型在预测集内的准确率分别为:SVM回归准确率为60%、决策树回归准确率为66.67%、Bagging回归准确率为60%、Boosting回归准确率为73.33%、Random forest回归准确率为73.33%。因此,我们认为2015年12月锌期货价格相对于2015年11月的综合上涨概率为20.92%,即为2015年12月锌期货价格相对于2015年11月锌期货价格上涨的概率为20.92%。在分析过程中,我们还可以得到预测过程中变量重要性前五的变量,重要变量指的是在分析过程,对分析结果起重要影响的分析变量,模型分析过程中,重要变量如表2所示。

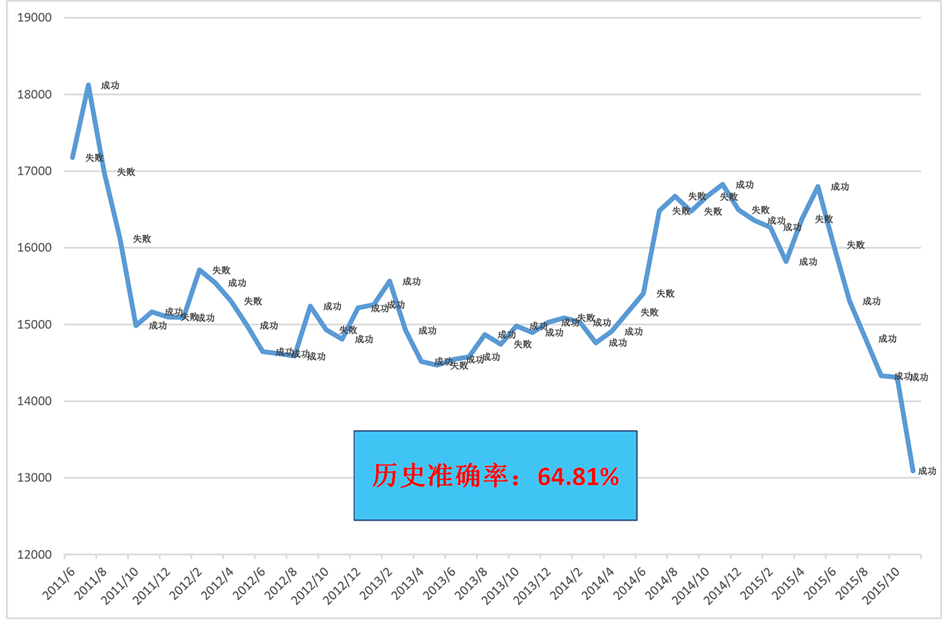

为考察模型在历史行情中的拟合情况,我们利用模型对2011年5月至2015年11月的期货锌月度价格的变动方向进行预测,预测结果如图1所示,可以发现,模型在2011年5月至2015年11月内预测准确率为64.81%,可以很好的对期货锌的涨跌方向进行预测判断。

4. 总结

可以发现,本文采用的五种模型中,有三种模型认为2015年12月锌期货的价格较2015年11月锌期货的价格下跌,结合5种模型在测试集中的表现情况,模型最终判断,2015年12月期货锌的价格相对于2015年11月期货锌的价格上涨的概率为20.92%,与历史行情相吻合,同时模型在预测过程中所用到的重要变量包括X2 (库存小计:锌:总计:月)、X8 (产量:镀层板(带):当月值)、X12 (70个大中城市新建住

Table 2. Important variables in lag one month prediction process

表2. 滞后一个月进行预测过程中的重要变量

Figure 1. Accuracy of model in lag one month prediction

图1. 滞后一个月进行预测过程中,模型的准确率情况

宅价格指数:当月同比)、X16 (沪伦比)、X20 (中国广义货币M2),均与铝的价格波动要较强的相关性,可以认为这5个变量对预测起关键性作用,同时结合历史数据发现,模型在历史行情中表现良好,预测准确率在60%以上,有较强的参考意义。