1. 引言

1.1. 研究背景

中国作为高碳能源大国,经济发展以高碳为显著特点,而目前世界正以低碳经济发展和环境保护作为新兴经济发展趋势,中国在新一轮的全球竞争中处于不利地位。无论是从国际还是国内来讲,发展低碳经济已经成为大势所趋。传统依靠手段实行节能减排的潜力已经越来越有限,市场机制将成为未来实行节能减排的重要途径。近百年来,全球变暖成为全球气候的显著变化,1992年5月联合国颁布了《联合国气候变化框架公约》,规定附件I的国家必须将2000年温室气体排放量下降到1990年水平。1997年12月在日本京都达成《京都议定书》,对温室气体排放量进行管制。《京都议定书》第17条规定了碳排放权交易,即附件I国家之间互相买卖碳减排配额的机制。欧盟排放交易体系在此基础上成立,并成为世界上最大的多边温室气体交易 [1] 。2010年中共中央在《国民经济和社会发展第十二个五年规划的建议中》指出要逐步建立碳排放交易市场。国家发改委也明确表示,“十二五”期间将逐步建立碳排放交易市场,鼓励和支持有条件的地区、行业探索碳排放权交易。2010年9月30日,以深圳成为国家首批低碳试点城市为契机,经深圳市人民政府批准,深圳排放权交易所成立。2011年上半年,国家发改委提出在北京、上海、天津、重庆、广东、湖北建立碳排放交易试点,逐步建立全国碳市场。

1.2. 研究意义及方法

目前,学术界普遍认为,石油价格是对碳价影响最大的外界因素。关于碳价格和石油价格的相互影响关系,目前已有很多讨论。传统的石油市场以汽油、柴油等生产生活主要用油为交易对象。随着新能源的发展和低碳机制的普及,传统的石油需求也随之呈现变动。因此,本文就现实状况,对国内碳市场交易价格和石油市场交易价格的交互作用进行计量分析,探讨碳交易市场和石油市场的历史变动对彼此的短期预测的影响。本文收集2016年5月6日至2017年4月28日共256个日度样本,选取北京碳交易成交价格和石油价格指数,构建VAR模型,研究国内碳市场交易价格和石油市场交易价格的动态关系。

2. 理论概述

2.1. 碳交易市场简介

碳排放权交易是根据各国政府实现对《京都议定书》的减排承诺的前提下,对本国企业实行二氧化碳排放额度控制的同时,允许其进行交易。碳交易的交易对象是交易主体用不完的碳排放额度。如果一个企业排放了少于预期的二氧化碳,则就可以将剩余的排放额度出售,而排放量超出配额的企业面临着由于超出排放而将得到的政府罚款,因此可以买入额外的碳排放许可限额,实现市场的交易 [2] 。

2.2. 碳交易市场与石油市场

生态环境问题突出,最主要的原因是巨大的化石能源消费以及长期以来的高碳、粗放的发展模式。2014年我国一次能源消费总量达到42.6亿吨标准煤,已成为世界第一能源消费大国 [3] 。中国当前巨大的能源消费总量和能源消费结构已给生态环境造成巨大压力,为解决严峻的生态环境问题,我国要实行的是重塑能源生产和消费模式,推动能源转型。因此,碳交易以控制碳排放为目的,其交易价格会对能源市场的价格产生影响。另一方面,发展清洁低碳能源,转变发展方式,减少能源市场的交易,提高能源使用的效率也会造成二氧化碳排放量的变化,对于以二氧化碳排放权为交易对象的碳市场交易价格也会受石油市场影响。

3. 文献综述

魏一鸣 [4] 关于欧盟碳市场与能源价格的关系进行实证研究。选取欧洲气候交易所的碳市场交易价格和德国欧洲能源交易所提供的石油价格数据进行协整关系检验,结果发现,能源价格与第一阶段碳期货价格之间关系较弱,而与第二阶段碳期货价格之间存在长期均衡关系,能源价格变化是推动第二阶段碳价变化的重要原因。魏瑞娟 [5] 采用协整检验考察了石油价格对碳排放的直接影响,以及碳价对碳排放的影响,发现在不可再生能源市场中,石油价格对碳排放的影响为负,碳市场在不可再生能源市场减排中具有积极作用。王惠敏 [6] 调查了1980至2010年中国经济增长、能源消费与碳排放的长期均衡、短期动态和格兰杰因果关系。协整检验结果表明经济增长、能源消费与碳排放之间存在长期的均衡关系。能源的短期波动会收到GDP和碳排放短期波动的影响。钟世和 [7] 研究了国际碳价、国家原油价格、国内石油价格与消费者价格指数之间的相互影响关系,得出了碳价是国际原油价格波动的原因,也是我国石油价格波动的原因,在《京都议定书》第一承诺期内碳价的波动对我国能源价格波动具有影响的结论。

根据已有的文献综述可以发现,鲜有关于国内碳交易市场价格的定量分析。中国的碳交易市场才刚起步,受政策影响较大,且中国的能源交易市场价格也受国际能源交易市场价格的影响,因此这也许就是对国内碳交易市场讨论较少的原因。因此本文以国内碳交易市场价格为研究对象,尝试对国内的碳市场价格进行定量分析。

4. VAR模型的理论构建与实证分析

4.1. 理论模型

向量自回归模型(VAR)是时间序列中自回归模型(AR)的延伸,把系统中每一个内生变量作为系统中所有内生变量的滞后值的函数来构造模型,描述的是在同一个样本期间内n的内生变量可以作为他们过去值的线性函数。本文中建立的VAR模型中包含两个内生变量,分别是碳交易市场交易价格(carbon)、石油市场交易价格(crude),构建的理论VAR模型如下页所示。

(1)

(1)

4.2. 数据选取与单位根检验

本文收集2016年5月6日至2017年4月28日共256个日度样本,变量为北京碳交易成交价格(carbon)和石油价格指数(crude)。其中,碳交易成交价格数据来源于碳k线网站,石油价格指数来源于卓创资讯,计量软件选择STATA和EVIEWS。

对原始数据做取对数处理以减小波动防止异方差的产生,对序列进行平稳性检验。

根据DF检验可知,碳交易成交价格为平稳序列,而石油价格指数不能通过单位根检验,为了建立VAR模型,需要对不平稳的序列进行差分。经计算,一阶差分后的序列达到了平稳状态。向量中变量的单位根检验结果如表1。

4.3. VAR模型的定阶

根据信息准则判断VAR模型的滞后阶数。STATA提供了VAR定阶的常用信息准则,其中常用的为LR似然比以及AIC、SIC信息准则。关于VAR模型定阶的结果如表2。

根据信息准则,LR和AIC支持滞后3阶为最佳滞后阶数,而SIC显示滞后1阶为最佳滞后阶数。因此对于两种滞后情况分别进行VAR模型估计并判断VAR的平稳性,通过VAR平稳性检验和VAR模型估计结果选择较优的模型作为最终选取的模型。

4.4. VAR模型估计与平稳性检验

4.4.1. 滞后一阶的VAR模型估计与检验

对于滞后一阶的VAR模型的显著性如表3。

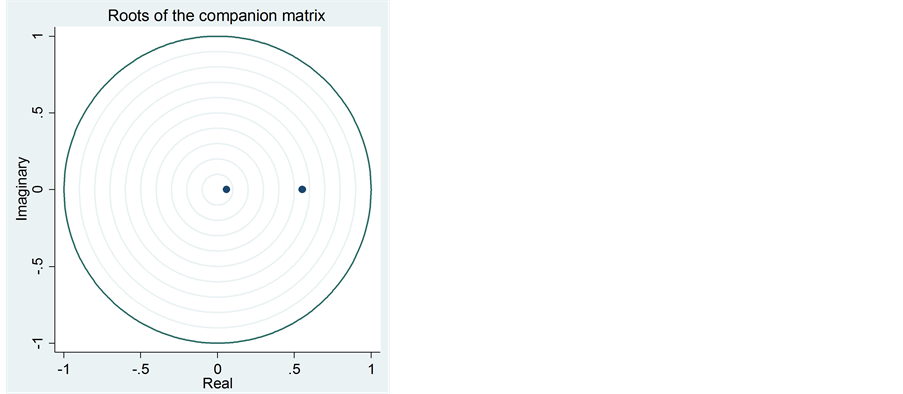

其中,VAR模型赤池信息准则AIC = −11.19995,施瓦茨准则SC = −11.11639。VAR模型的平稳性检验如图1所示。

4.4.2. 滞后三阶的VAR模型估计与检验

对于滞后三阶的VAR模型的显著性如表4。

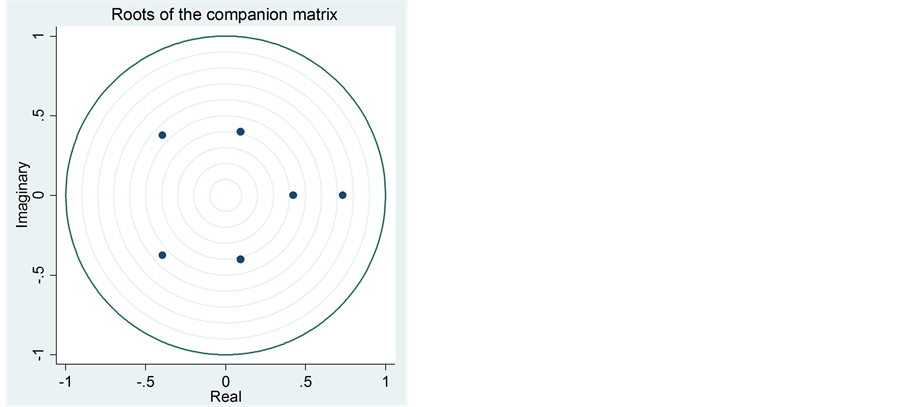

其中,VAR模型赤池信息准则AIC = −11.28419,施瓦茨准则SC = −11.08812。VAR模型的平稳性检验如图2所示。

由此可见滞后三阶的VAR模型的单位根都在单位圆内,模型平稳,且两个方程都是显著的,因此本文选取滞后三阶的VAR模型作为研究对象。因此可以构建VAR模型如表5。

4.5. 脉冲响应函数分析

建立脉冲响应函数的结果如图3所示。

根据脉冲响应的输出图形可以看出,首先,碳交易价格的脉冲对自身在当期影响最大,之后逐渐平稳。当石油价格指数的变化率给碳交易成交价格一个单位的正冲击时,碳交易的成交价格在第三期的时间呈现小幅正向波动,之后出现下降,逐渐趋于平稳状态。而当碳交易成交价格给石油价格指数变化率一个单位正冲击时,石油价格指数变化率会存在小幅上升,在第二期呈现最大,滞后逐渐平稳。

根据脉冲响应的结果,可以验证,碳交易价格和石油价格指数的相互影响是存在的,且都是对对方产生正向影响,但影响出现的滞后时间不同。碳交易价格对石油价格指数变化率的影响是即刻发生,而石油价格指数变化率对碳交易价格的影响在两期后才显示出来。

Table 1. Result of unit root test of series

表1. 序列的单位根检验结果

Table 2. Information criterion of VAR model

表2. VAR定阶的信息准则

Table 3. Significance level of VAR model lag (1)

表3. 滞后一阶的VAR模型的显著性

Table 4. Significance level of VAR model lag (3)

表4. 滞后三阶的VAR模型的显著性

Figure 1. Result of unit root test of VAR lag (1)

图1. 滞后一阶的VAR的单位根检验结果

Figure 2. Result of unit root test of VAR lag (3)

图2. 滞后三阶的VAR的单位根检验结果

Table 5. Estimated result of VAR model

表5. VAR模型估计结果

4.6. 方差分解

通过方差分解,可以分析出各变量的滞后期对目标变量波动的贡献率,从而反映每个内生变量的随机冲击在VAR系统中的相对重要性。

4.6.1. 各变量对碳交易成交价格的方差贡献

碳交易成交价格的方差贡献如表6所示。

根据方差贡献结果可以看出,碳交易成交价格在第一期只受自身波动影响,第二期开始显现出石油价格指数变化率的方差贡献。在第四期,碳交易成交价格受自身影响的方差贡献保持在97%左右,石油价格指数变化率的影响保持在3%左右。

4.6.2. 各变量对石油价格指数变化率的方差贡献

石油价格指数变化率的方差贡献结果如表7所示。

石油价格指数的变化率在第一期受自身99.9%的影响。从第二期开始,碳交易成交价格的影响开始显现,最终保持在7%左右。

通过方差分解的结果可以看出,碳交易成交价格和石油的价格指数变化率都是受自身影响的相对比率较大。而相互影响作用虽然存在,也不足10%。从定性的角度来看,可以确定两者的滞后期都会对彼此的当期产生正向影响,但关于相对影响比率不大的原因,可以归结为两点。第一,为了建立VAR模型,对于不平稳的序列需要进行差分,因此对于石油市场交易价格变为石油价格指数的变化率。对于变化率对碳市场成交价格的影响肯定不及价格指数的影响明显。第二,中国正处于碳交易的起步阶段,作为传统的碳排放大国,中国还是更加依靠传统的能源进行生产生活活动。因此碳交易市场的成交很大部分的影响是由于政策,碳市场交易还不能称为一个灵活的完全交易市场,因此碳市场的价格变化本身的规律性不太明显。

Table 6. The variance decomposition of carbon trading transaction price

表6. 碳交易成交价格的方差分解结果

Table 7. The variance decomposition of change rate of gasoline price index

表7. 汽油价格指数变化率的方差分解结果

5. 结论分析

本文从已有的研究结论出发,探讨石油价格与碳价的互动关系。碳交易是控制碳排放的手段,而传统的能源市场也会对碳交易产生影响。本文选取代表碳市场交易价格的北京市碳交易成交价格、代表能源市场交易价格的石油价格指数作为变量,建立向量自回归模型。根据VAR模型的建立条件,对石油价格指数作一阶差分,进而研究碳交易价格、石油价格指数变化率的VAR模型。根据信息准则和VAR建模的结果以及平稳性检验,确定VAR模型以滞后一阶的形式为最佳。之后进行脉冲响应函数分析以及方差分解。可得出以下结论。第一,碳交易成交价格受大部分自身影响,而随着时间的推移,石油价格指数变化率对碳交易成交价格的影响逐渐增加。第二,石油价格指数变化率受自身影响较大,而碳交易成交价格的影响存在,维持在7%左右。

通过实证分析的结果可以总结出现实的碳交易市场与石油交易市场的特点如下。首先,国家为了减排,出台了一系列加大科技创新投入、增强可再生能源开发利用的环境政策,因此对能源市场,特别是石油市场是有政策冲击的。但作为传统的能源消耗大国,我国的节能减排正处于初级阶段,以风能、太阳能和生物质能等为主导的可再生能源市场并不具有非常强的代表性,因此传统的能源市场仍然处于主导地位,碳市场是否有效仍然需要进一步观察。碳市场的建立仅仅是节能减排的途径之一,而中国建立的碳市场除了深圳、北京、上海等地的试点时间超过两年,其他的碳交易试点的交易量仍然不是很多,这说明中国国内参与碳交易仍然不是一个常用的交易市场,关于国内碳市场的定价机制也并没有完全公布,国内的碳市场受政策影响较大。因此本文的研究主要出于理论化,实证分析的结果仅仅是一方面参考。

中国的碳交易市场才刚刚起步,碳交易市场的卖方主要是以拥有能吸收二氧化碳能力的自然资源,如森林、草地等的国有企业。而对于买方,由于采取的是自愿市场的交易形式,相当一部分排放超过限额的企业并没有加入到碳交易市场中来,因此对于碳交易市场的价格并不能完全的反映市场价格,因此碳交易市场的价格较平稳。所以可见,对于中国的碳交易市场,需要更积极的政策和规定来刺激更多的企业加入碳交易市场,这是对实行节能减排,缓解环境压力的重要举措之一。