1. 引言

随着以互联网为代表的现代信息科技的发展,互联网金融模式已经成为既不同于传统商业银行间接融资、也不同于资本市场直接融资的新型融资模式,从2007年,P2P网络借贷进入中国开始,其逐渐成为互联网金融模式的主要代表之一 [1] 。P2P (Peer-to-Peer)网络借贷主要是面向个人借款者或中小企业者的贷款,P2P网络平台作为中介平台,让具有闲置资金并有意愿借款的个人或中小企业发布借款信息,出借者选择利率和到期时间满意的项目,撮合成交 [2] 。

P2P网络借贷作为借贷业务的一种,所面临的最大风险就是信用风险。信用风险是借款人因各种原因未能及时或足额偿还债务的可能性。近年来P2P网络借贷在中国发展十分迅猛。截止2015年8月,全国P2P网贷行业总体成交量达到974.63亿元,正常运营平台2283家。但由于网贷平台发展速度快,信用风险管理相对滞后,问题平台频频出现。截止2015年8月,累计问题平台已有976家。这些问题平台中,除了部分存在恶意欺诈外,更多平台都是因为对借款人的信用风险控制不严,出现坏账难以及时处理,然后遭遇挤兑,最终导致平台破产。尽管各平台尽可能审核借款人的身份信息和其它真实资料,来进行信用风险评估,但违约现象仍大量存在。所以,能否准确有效的评估P2P网络借贷平台个人借款者的信用风险,尽量减轻其带来的负面效应,是目前P2P网络借贷平台自身以及监管当局关注的热点问题。

P2P网贷公司规模普遍较小,其风险管理能力远低于传统商业银行等金融机构,但P2P网贷的借款项目质量偏低,这就需要其具备较强的风险管理能力 [3] 。目前,P2P网络借贷平台对于借款人的信用风险,主要措施通常有以下几种:第一,加强借款人信息的审核,当借款人申请贷款时,平台会要求提供详尽、真实的个人信息,并通过实地认证或视频认证等方式进行认证 [4] ;第二,限制金额和期限。目前P2P网络借贷平台一般根据信用评级规定借款额度上限,借款人借款额度不得超过该上限,在期限方面,比如Zopa平台,要求借款人按月分期还本付息,以减轻借款人的还款压力,降低违约风险 [5] ;第三,提供信用评级。Iyer等研究发现出借人主要依靠标准的银行征信系统信息来推断借款人的信用情况 [6] 。目前,我国P2P网络借贷平台的信用风险管理主要运用信用评分模型进行。平台通过借款人信息计算出一个分数,代表借款人的信用风险,以此确定信用评级 [7] ;第四,提供担保。对贷款提供担保或是平台自身建立保险制度,当借款人出现违约时,担保人或平台先行偿付本金,减少因借款人违约对出借人造成的损失。国外Prosper平台引入“背书”评价制度,借款人可以邀请朋友为其背书,证明其信用,背书内容会在借款人信息上显示 [8] 。

纵观上述P2P网络平台个人借款者信用风险的管理仍存在很多问题。首先,各个P2P网络借贷平台建立的信用评级各异,没有一个系统的信用风险评估机制,这是P2P网络借贷风险最大的风险隐患;其次,大多数P2P网络借贷的借款利率一般都较高,在10%左右,高昂的借款利率增加了借款人的违约率;第三,对借款人还款能力没有进行预评估。本文将结合P2P网站人人贷可观测到的特征变量(人口特征、职业状况、收入财产、历史信用、操作认证),参考传统商业银行个人信用风险评价指标体系,建立适用P2P平台个人借款者信用风险评价的指标体系,然后利用BP神经网络模型评估个人借款者信用风险,再针对P2P网站经常存在信息缺失的情况,研究信息缺失情况下模型的准确程度,利用多次仿真得出平均模型识别准确率与较优模型识别准确率比较,检验模型的稳健性。

2. BP神经网络原理

2.1. BP神经网络算法概述 [9]

BP神经网络(Back Propagation)也可称为误差反向传播网络,最早是由Werbos在1974年提出来的,1985年Rumelhart等发展了该理论,提出了清晰而又严格的算法。BP算法适用于前向网络,它采用有导师学习的训练形式,提供输入矢量集的同时也提供输出矢量集,通过反向传播学习算法,调整网络的连接权值,以使网络输出在最小均方差意义下,尽量向期望输出接近,反向学习的进程由正向传播和反向传播组成。在正向传播过程中,输入信息经隐含神经元逐层处理并传向输出层,如果输出层不能得到期望的输出,则转入反向传播过程,将实际输出与期望输出之间的误差沿原来的连接通路返回,通过修改各层神经元的连接权值,使误差减小,然后转入正向传播过程,反复循环,直至误差小于给定的值为止。

2.2. BP神经网络算法在我国P2P网络借贷平台个人借款者信用风险评估中应用的可行性

首先,P2P网络借贷作为现代信息社会的新事物,目前尚未建立系统有效的信用风险评估机制,对个人借款人信用风险的评估很不完善。而BP神经网络具备自我调节,高度自学的特点,灵活性强,可以使其随环境的变化不断调整,从大量复杂的数据中发现规律,并根据这些规律给出相对正确的推理结果。所以,BP神经网络对P2P网贷中信息不确定,并缺乏系统有效评估机制的借款人信用风险评估具有较强的实践可行性。

其次,BP神经网络可以再现专家的知识、经验和思维,最大程度剔除评估时的主观性,这样可以使信用评估更为准确。

最后,BP神经网络模型是一个非线性建模过程,并且不需要探究数据之间存在哪一种非线性关系,所以,可以有效克服传统建模过程中选择适当的模型函数形式的困难,能够十分快捷地建立模型,应用更加方便广泛。

3. 建立P2P网贷个人信用风险评估模型

3.1. P2P网络借款平台个人借款者信用风险评估指标选取

P2P网络借贷平台一般要求借款人提供的个人信息是其身份信息、职业状况、资产状况等个人基础情况,然后通过实地认证和视频认证等方式对借款人提供的信息进行认证,以保证其信息的真实性,根据认证后的信息对借款人信用等级进行评定,并将信息及信用评级结果公布在网站上,供资金出借人参考。故本文根据P2P网络借贷的特点、人人贷网站可观测的数据及传统商业银行个人信用评级指标选取原则,将借款人的基本资料归纳为人口特征、职业状况、收入财产、历史信用、操作认证等5个方面。

本文参考商业银行个人信用评级取值标准,结合P2P网络平台的特点,以及各个指标对于信用评级的重要性,对5个方面信用评估指标进行信用风险量化,指标选取及取值理由如下:

(1) 人口特征。人口特征包括年龄,婚姻状况和文化程度。年龄:不同年龄阶段的借款人的违约率有较大差别。一般,35岁至50岁,工作较为稳定,经济状况良好,其违约率低;26~35岁的借款人,收入开始增加,但家庭负担开始增大,其违约率一般;低于25岁的借款者,收入不高,缺乏良好的消费习惯,大都没有储蓄能力,其违约风险高;而年龄大于50岁的借款人,收入水平开始下降,突发消费较多,其违约风险也相对较大。婚姻状况:已婚的借款人情况较为稳定,而离婚和未婚的借款人信用状况可能偏低;文化程度:一般而言,文化程度越高发生违约几率越低。

(2) 职业状况。职业状况包括单位类别,岗位类型和工作年限。单位类别:一般而言,政府机关职工收入水平稳定,违约的可能性越小,故其取值最高;企业规模越大,收入水平越稳定,违约率越小;岗位类型:岗位越高,收入水平越高,违约风险越小;工作年限:工作年限越长,收入水平越稳定,违约风险越小。

(3) 收入财产。收入:收入越高,违约的风险越小;房产:在我国,住房条件通常代表个人的经济能力,所以有房产的比无房产的违约风险小;车产:车也代表着个人的经济能力,所以有车的更不容易违约。

(4) 历史信用。历史信用主要通过成功还款次数和逾期还款次数反映。成功还款次数:成功还款次数越多,说明其信用惯性越好,越不容易违约;逾期还款次数:逾期笔数多,说明其历史信用不好,历史信用不好的借款者更容易违约。

(5) 操作认证。认证的种类越多,说明其信息更真实、完整,违约的可能性越小。

参考银行个人信用评级取值标准,结合P2P网络平台的特点,具体取值如表1,指标取值越高,信用级别越高,违约的可能性越小。

3.2. 数据收集与处理

3.2.1 数据收集

本文从人人贷网络交易平台交易数据中选取164名无违约记录的借款人信息和4名有违约记录的借款人信息,共168组数据作为P2P个人借款者信用风险评估的样本。样本选取截止时间是2015年9月10日。根据表1将个人信用指标中的定性指标转化为定量数据,转化后的168组个人信用指标定量数据见附件1。

3.2.2. 数据归一化处理

一般而言,神经网络的样本输入数值需要进行归一化处理。本文通过最大最小值法对个人信用指标定量数据进行归一化处理,即运用式(1)进行归一化,最大最小值法归一化是一种线性变换,不会造成信息的过多丢失。

(1)

(1)

3.2.3. 数据分析

对选取的数据关于各个指标做基本特征分析。简单统计分析结果见表2。

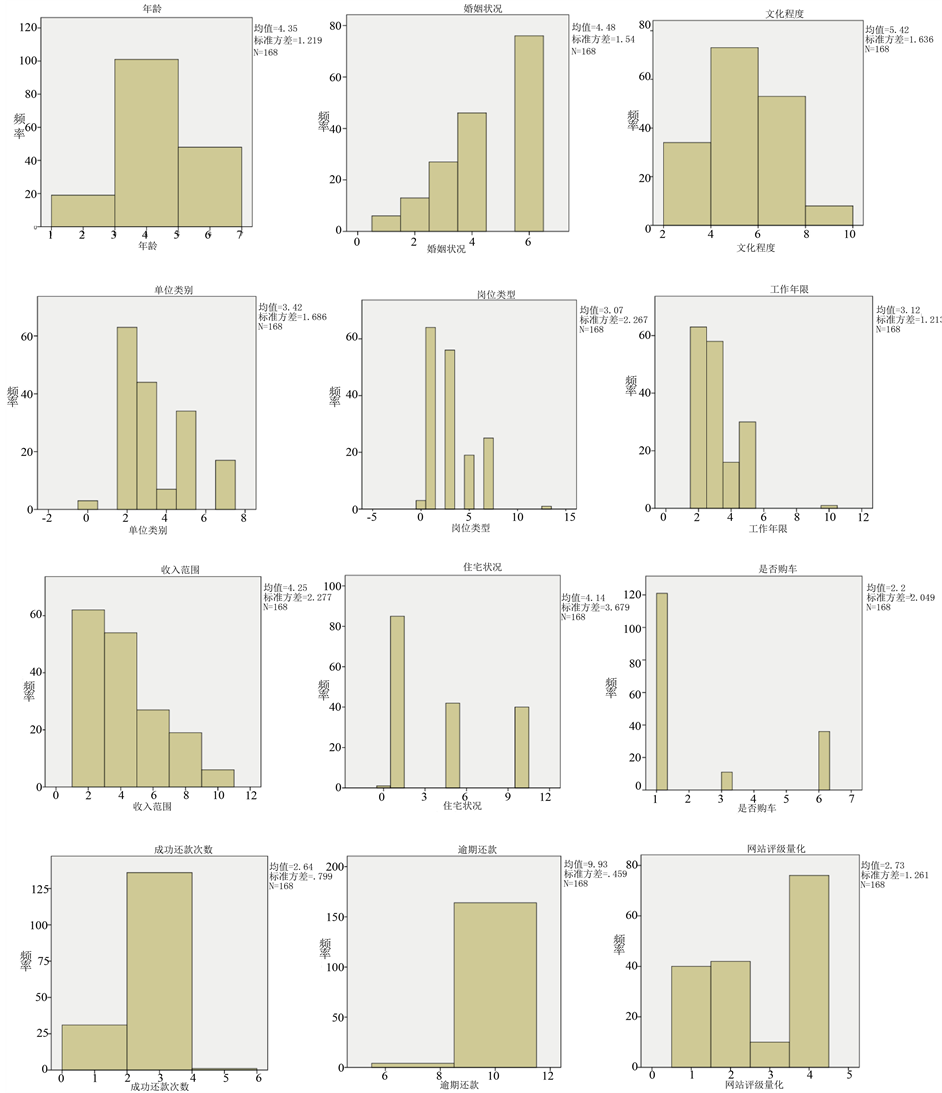

将表2中均值与极大值和极小值比较以及其他基本统计指标,可以看出本文选取的样本较有代表性。利用SPSS软件作出样本量化数据的频率分布直方图见图1。

从图1中可以看出,本文选取样本数据时,在结合实际网站情况下,也基本考虑了样本各个指标的分布情况,选取样本较具有代表性。

Table 1. P2P network lending platform for personal credit evaluation index value

表1. P2P网络借贷平台个人信用评估指标数值化

Table 2. Simple statistical analysis of sample data

表2. 样本数据简单统计分析

Figure 1. Frequency distribution histogram of sample data

图1. 样本量化数据的频率分布直方图

3.3. 模型的构建

本文采用三层神经网络模拟P2P网络借贷平台个人信用风险评估过程,如图2所示。

输入层节点数为12,分别为年龄、婚姻状况、文化程度、单位类别、岗位类型、工作年限、收入范围、住房状况、车产状况、成功借款次数、逾期还清次数、操作认证。

输出层为P2P平台个人借款者信用等级,虽然人人贷将信用评级结果分为AA、A、B、C、D、E、HR共七类,但只有A、D、E、HR这四个信用等级有较多的借款者,所以模型输出层只取四个信用等级。输出层节点数为1,取值分别为4,3,2,1,分别对应四个信用等级,信用等级A取值为4,信用等级最高,其违约的可能性越小,取值为3的信用等级次之,信用等级HR取值为1,等级最低,最有可能违约,不能及时还款。

隐层节点数一般先根据黄金分割法确定节点数大致范围,再经过试验确定最优隐层节点数。

3.4. 模型仿真

3.4.1. 训练过程与结果

在仿真过程中,用168条数据中前150条数据作为训练数据,并进行拟合,训练数据中含有147个违约借款人和3个无违约记录的借款;将第151至168条数据作为测试数据,其中违约借款人样本为1个,无违约记录的借款人样本为17个。使用train函数来训练创建的BP神经网络,设置训练步长为500,逾期误差目标是0.001,经试验,最优隐层节点数为6。

由图3可以看出,经过500次迭代后,达到预期误差目标0.001。BP神经网络模型训练时间较短,

模型较优。

模型训练运算结果拟合图见图4。由图4可以看出,BP神经网络模型在训练过程中的误差较小,拟合情况良好。

3.4.2. 仿真过程与结果

训练及拟合完成后,对经过训练生成的祌经网络模型的预测结果进行验证。

输入测试数据151至168条验证数据后,目标输出结果与模型输出结果对比见表3,其中目标输出为网站对个人借款者的评级,模型输出结果为BP神经网络仿真结果。表3为部分借款人目标输出与模型输出结果。

模型仿真结果四舍五入得到评级输出结果,将评级输出结果与目标输出结果对比,模型识别的准确率为83.3%。由表3和模型识别率可以看出,模型根据150个借款人数据进行训练和学习后,在模型预测的输出结果和目标输出结果基本一致。由此可见根据BP网络的算法思想建立的P2P网络信贷借款人信用风险评估模型,通过人人贷网络借贷平台个人基础信息和信用历史数据的训练和学习,调整模型权值和阈值,确定输入层和输出层的关系,从而使模型具备了对P2P网贷个人借款者信用风险的预测评估能力,且评估的准确率较高。

3.4.3. 数据缺失的仿真结果验证

由于P2P网贷平台的信息是由借款人自主录入的且未有强制性,可能会存在借款人部分信息缺失,或者借款人故意隐瞒或欺骗导致部分信息错误的情况,因此在对P2P网贷平台个人借款者评估信用风险时,会存在部分缺失或无效信息。BP神经网络模型特点之一就是在部分数据缺失的情况下,依然能够通过之前训练结果给出较为准确的评级结果。本文分别剔除151至168条数据中输入层的12个指标后,对模型的预测结果进行验证。在信息缺失的情况下,目标输出与模型输出结果对比见表4。

从表4信息缺失情况下模型输出结果与目标输出结果对比情况来看,在年龄信息、婚姻状况、文化程度、工作年限、住房状况和车产状况缺失的情况下,虽相较于信息完整的模型输出结果有一些差距,

Table 3. Comparison between target output and model output

表3. 目标输出与模型输出结果对比表

Table 4. Comparison between target output and model output in data missing situation

表4. 目标输出与模型输出、数据缺失情况结果对比表

但整体模型输出结果与目标输出仍基本一致;在单位类别、岗位类型和收入范围信息缺失的情况下,模型输出结果与目标输出结果有较大的差距;在成功借款次数、逾期还款次数、操作认证信息缺失的情况下,模型输出结果与目标输出结果差别大,但未出现逆转性结果,即信用风险较低的借款人不会被判断为信用风险较高借款人。故仍可以作为对P2P网络信贷中借款人信用风险评价的依据。由此可见,在信息模糊缺失的情况下,BP神经网络模型仍具备对P2P网络信贷借款人信用的预测评估能力,且评估的准确率仍然较高。

4. 结果分析和建议

本文利用BP神经网络模型建立的P2P网络信贷借款人信用风险评估模型验证情况良好,即使在部分信息缺失或模糊的情况下,仍能对借款人的信用风险做出较为准确的判断,具有较强的预测评估能力且具有一定的适用性,可以推广使用。本文的BP神经网络信用风险评估模型具备很强的评估能力的原因,主要是BP神经网络本身具有很好的知识发现和特征抽取能力,十分适合信用风险类的评估,总体实验结果证明了BP神经网络适用于P2P网络借贷个人借款者信用风险评估。

基于以上研究结论以及个人信用风险评估内外环境的要求,本文提出完善P2P网络借贷平台个人借款者信用风险评估、促进P2P平台健康发展的对策和建议:

第一,加强P2P网络借贷平台信息认证,保证个人信息的准确性。P2P网络借贷平台对借款者的评级需要借助借款者所提供的信息,信息的真实、准确是评级的关键,网站应对借款者提供的信息进行实地认证或证件认证,避免错误信息导致错误评级,损害贷款者的利益。

第二,增加P2P网络借贷平台信息的披露。更多的个人信息有利于贷款者对借款者的全方位了解,也更加有利于网站对于借款者的信用评级。

第三,P2P网络借贷平台应及时披露逾期还款名单。逾期还款的次数对于信用评级是至关重要的,及时披露,调整信用评级,有利于贷款者准确的了解借款者的情况。及时的逾期披露也给借款者带来了一种无形的压力,促使他们及时还款,重视信用。

致谢

感谢我的导师李淑锦老师对我论文悉心的指导和耐心的修改。感谢杭州电子科技大学让我申请到杭州电子科技大学研究生科研创新基金项目,让我可以拥有更多科研的条件和资源。感谢同专业、同学院的同学,在我研究生学习期间帮助我、启发我、鼓励我,使我不断进步。感谢父母、家人一直在身边支持我,让我更安心的研究感兴趣的课题。

附件1:样本数据

续表

续表

续表

续表

续表